The Fixed Income Brief: Pow Pow(ell)

Better jobs data and worse inflation data push the Fed to accelerate tapering as the market prices in an earlier hike in 2022.

December 12, 2021

Fixed Income Trivia Time:

The first credit agency was created due to what financial crisis?

Next week, the Fed is expected to accelerate the tapering of its bond-buying program, likely reducing its purchases by $30bn a month rather than $15bn that was originally assumed. This in turn has fixed income investors pricing in a more aggressive Fed, with the expected likelihood of a hike moved forward to May 2022.

Gauging the progress in the recovery of jobs since the pandemic is critical now as the Federal Reserve changes gears on its ultra-easy monetary policy and prepares its first normalization steps after more than a year and a half of unprecedented accommodation. Initial filings for unemployment insurance totaled +184k for the week, the lowest going back to September 6th, 1969. The total number of people receiving benefits under all programs dropped as well, lower by -350k to 1.95mil, about ~10x that level a year ago. At the moment, it is less clear the recovery is fully complete as the above trend in claims contradicts the weaker-than-expected monthly payroll numbers from last week that disappointed markets. November’s non-farm payroll showed hiring growth of just 210,000, well under expectations even with the unemployment rate sliding to 4.2%. There is a chance Powell and the Fed use the full lack of clarity to not be overly hawkish, but the market certainly will expect a significant change in the committee’s tone.

The more pressing driver for Fed action remains the stubbornly high inflation figures. Friday’s CPI release supports recent market sentiment that the Fed will now need to take more aggressive steps to combat price increases. U.S. November Core CPI increased +0.5% MoM and +4.9% YoY as expected by the market. The headline YoY figure is up +6.8%, up from +6.2% in October, and slightly higher on the MoM basis than the market expected, the highest level since the summer of 1982.

Volatility picks up ahead of Fed meeting, rates end higher WoW

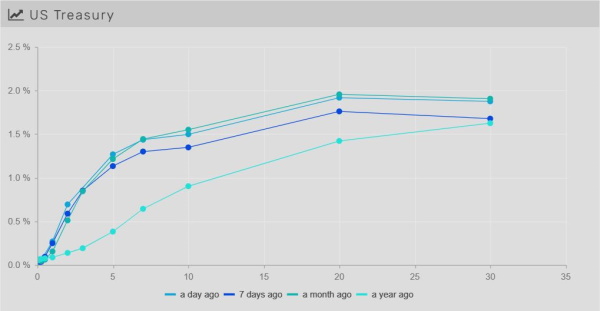

The benchmark 10yr U.S. Treasury bond traded in a ~15bps range this week, ending higher towards the top of the recent range at 1.48%. The 2yr note linked more closely to Fed policy moved higher by +13bps on an intraday basis, but closed off the high to end +7bps WoW at 0.66%. The price action in Treasuries overall was driven by a shift in the expected chances of seeing the first hike in May vs. July as the Fed is set to meet next week to lay out their strategy to unwind open market purchases.

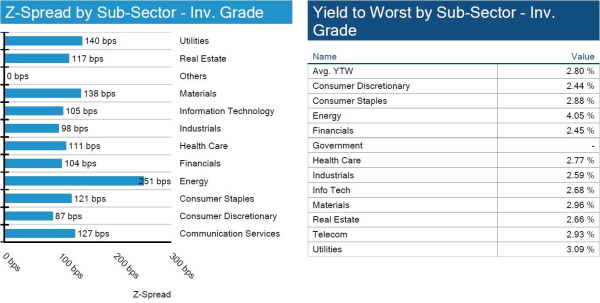

IG spreads continue to reflect future concerns from Fed action

Credit spreads move wider as expectations settle in for more widening. Yields on the long end are lower and real bond yields are expected to move higher.

High yield continues to outperform IG

HY is outperforming IG MTD by ~140bps bringing the YTD difference to 348bps. The driver continues to be a reduction of the overall default rate to pre-pandemic lows.

Portion of Qualcomm’s debt sees upgrade

Qualcomm was upgraded to single-A on broadening their revenue stream and increasing growth trajectory.

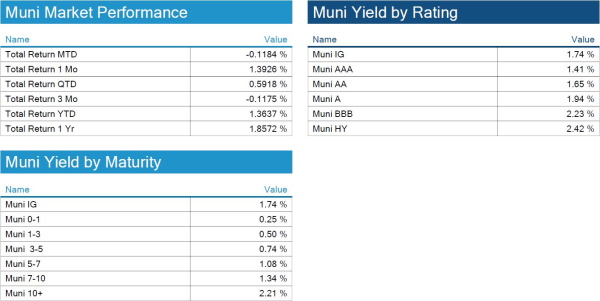

Munis close out an already busy year on a high (supply) note

The municipal bond market is headed out of 2021 with a rush of issuance, but still not enough to keep up with the insatiable amount of demand. Issuance is expected to be about $21bn over the next 30 days, with most of that front-loaded to the next two weeks, led by a $4.2bn CA tobacco deal. The current visible supply is the highest the market has had YTD, which is typical given syndicate desks are trying to get things out the door before year-end, but also ahead of an expected more aggressive Fed in 2022. The issuance will be welcome by the market though as investor cash balances are heavy at the moment. Is it enough supply to cheapen muni spreads? Check back next week for the answer.

*Disclosure on all charts: Figures shown above are the weighted aggregate of bonds that currently have an IDC price and based on transactions over the past 2 weeks. This may create anomalies in the data but aligns with our effort to reflect actual market conditions. Data pulled as of end of day Thursday, December 9, 2021.

View full IG, HY, and muni market reports pulled from IMTC:

Fixed Income Trivia Time:

The financial crisis of 1837. Lewis Tappan established the first agency in 1841

Want to get this in your email every Sunday? Sign up to receive The Fixed Income Brief weekly.

This paper is intended for information and discussion purposes only. The information contained in this publication is derived from data obtained from sources believed by IMTC to be reliable and is given in good faith, but no guarantees are made by IMTC with regard to the accuracy, completeness, or suitability of the information presented. Nothing within this paper should be relied upon as investment advice, and nothing within shall confer rights or remedies upon, you or any of your employees, creditors, holders of securities or other equity holders or any other person. Any opinions expressed reflect the current judgment of the authors of this paper and do not necessarily represent the opinion of IMTC. IMTC expressly disclaims all representations and warranties, express, implied, statutory or otherwise, whatsoever, including, but not limited to: (i) warranties of merchantability, fitness for a particular purpose, suitability, usage, title, or noninfringement; (ii) that the contents of this white paper are free from error; and (iii) that such contents will not infringe third-party rights. The information contained within this paper is the intellectual property of IMTC and any further dissemination of this paper should attribute rights to IMTC and include this disclaimer.

.

.

Related articles

January 6, 2025