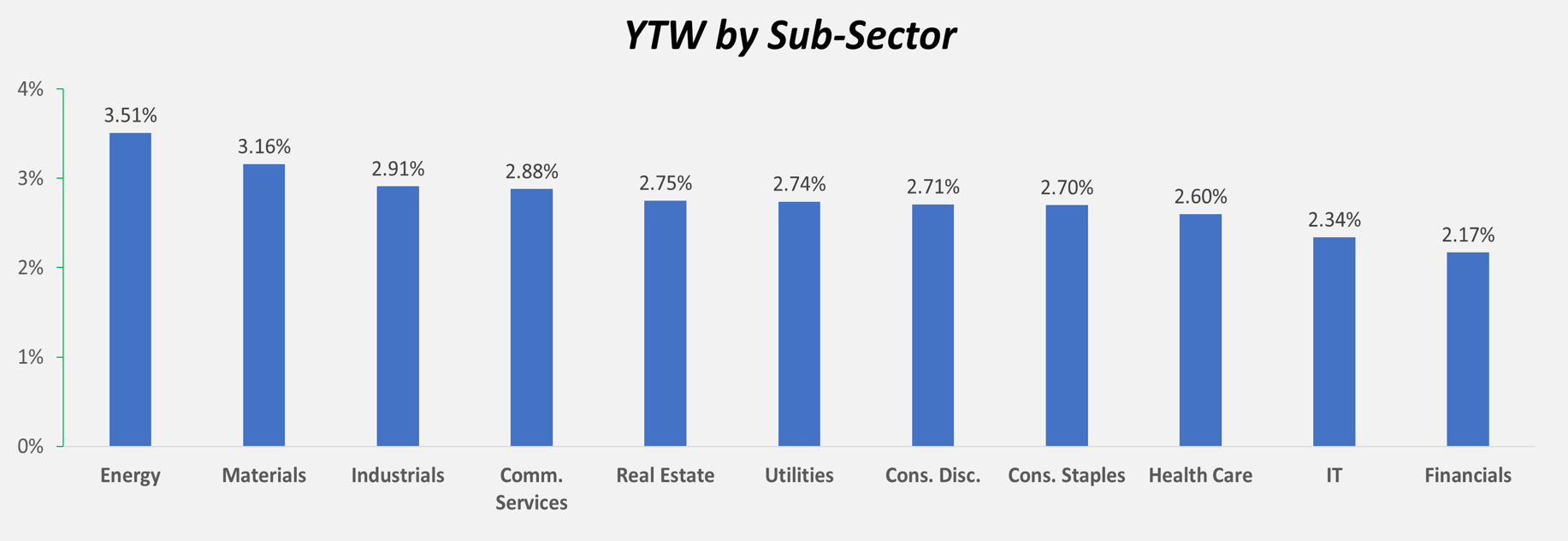

Stocks reversed multiple weeks of recovery, selling off four out of the last five days to post one of its worst weeks since March. As the risk off tone gripped the markets, Treasury prices rallied causing the yield on the 10-yr benchmark Treasury to move lower by -25 bps towards its near-term average of 0.65%. Total returns of both the Bloomberg Barclays U.S. Aggregate and U.S. Corporate Bond Index were higher but underperformed U.S. Treasuries on an excess return basis. This week we are back to monitoring test results more closely across the U.S. as states in the northeast continues to slowly open their economies. Given the recent poor approval ratings of President Trump, the market should not be surprised by an announcement by the Treasury Department to provide additional stimulus here.

The Fed reduces future growth forecasts and urges additional government stimulus

The Federal Reserve kept rates unchanged last week and reiterated its commitment to keep rates unchanged through 2022. The Fed stated, “the committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” The decision comes as the central bank continues to roll out its lending programs to support the economy, which officially entered a recession in February, data earlier this week showed. Despite the recent surprise in U.S. hiring in May, the Fed slashed its growth forecasts for the years ahead amid uncertainty over the impact from the pandemic. The economy is expected to contract by 6.5% in 2020, but up by 5% next year, and 3.5% in 2022. The unemployment rate for the year is expected to come in at 9.3% though expected to fall to 5.5% by 2022. The pace of inflation, which will continue to be the key driver for future monetary policy, is forecast to cool to a rate of 0.8%, down from 1.9% previously. Additionally, core-PCE inflation for 2021 was revised lower to 1.5% from 2%.

The wave of stimulus from the Fed has taken its balance sheet above $7 trillion from about $4 trillion just before the pandemic struck in the U.S. in early March. Despite this, the central bank has no plans to rein in quantitative easing, pledging to maintain the current pace of bond purchases over the coming months to support the flow of credit to households and businesses. Purchases over the coming months will be made across a range of debt including Treasuries, agency residential, municipals, and commercial mortgage-backed securities.

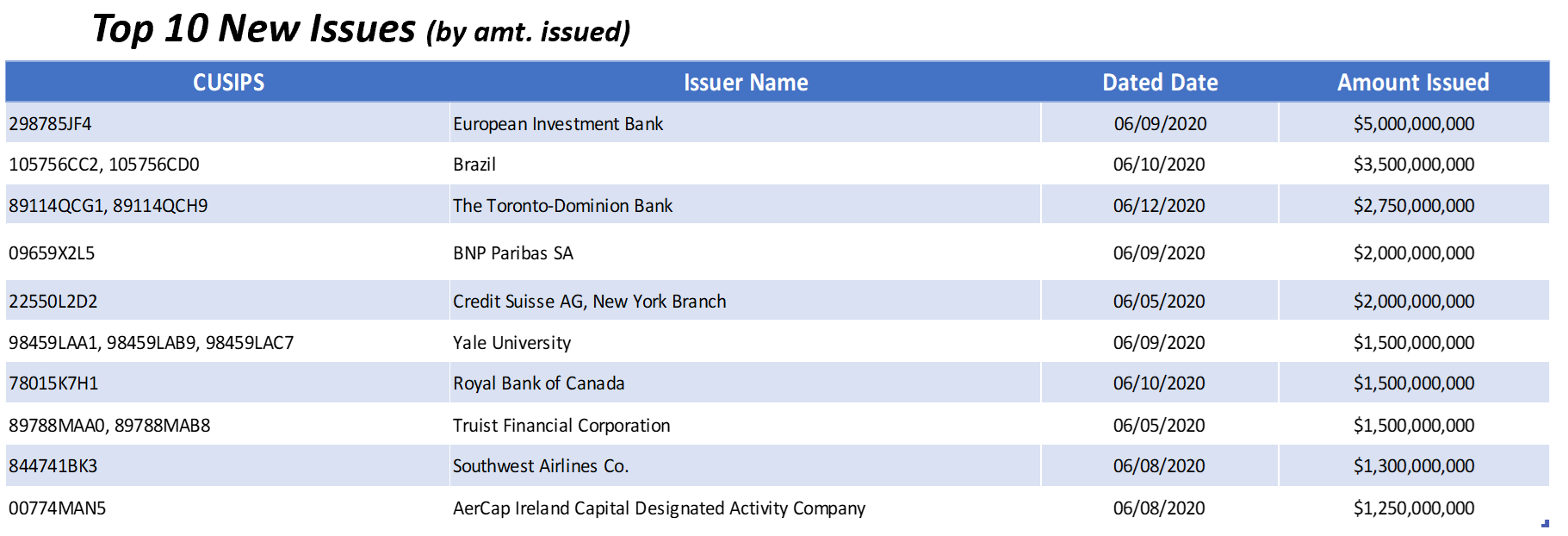

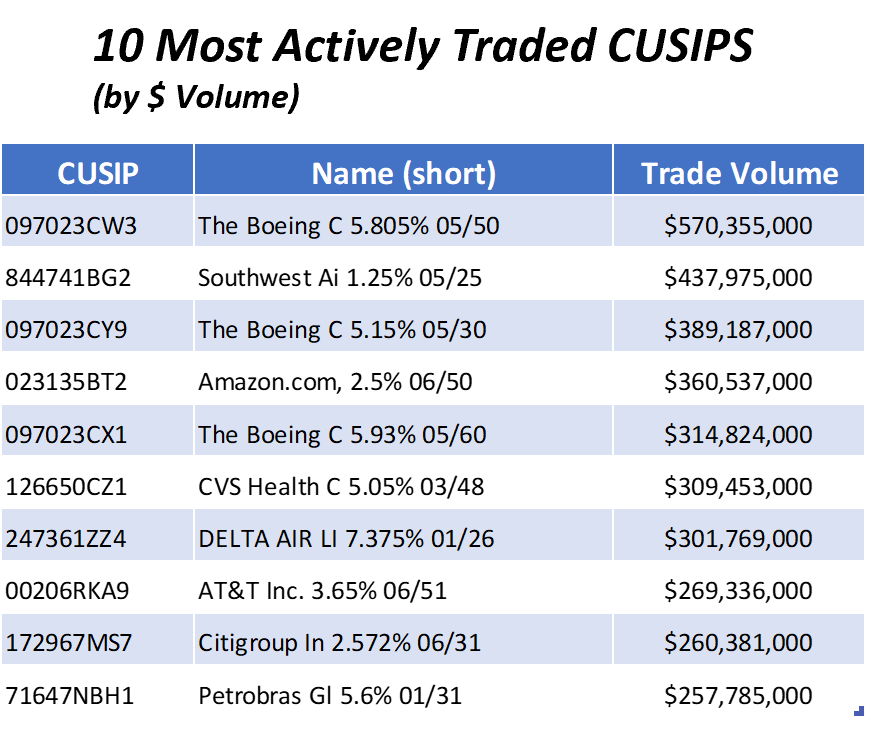

Muni market remains strong amidst weaker risk tone

Strong interest continues in the municipal bond market as numerous new deals are seeing significant oversubscriptions. Investors are expecting summer supply and demand technicals to remain tight with June redemptions coming in at $40bn and total summer redemptions forecast to total $120bn. New issuance may not be able to meet demand based on expectations of lower new issue visible supply in the summer months ahead. Issuers are able to take advantage of investor appetite by issuing at lower yields, which may draw in more issuer interest but there is a sense that it still will not be enough to offset the cash available on the sidelines. Allocations are set to remain poor across the board as cash continues to find its way back into muni bond funds after the $40bn that had left at the peak of the COVID outbreak.

Key indicators for the week ahead

Federal Reserve Chairman Jerome Powell is due to testify to Congress on Tuesday and Wednesday amid concerns over a possible resurgence of COVID-19 cases. U.S. retail sales data will be watched for indications on the strength of the reopening rebound. The latest initial jobless claims report will be released on Thursday. Jobless claims totaled 1.5m last week, marking the 10th consecutive weekly decline of jobs, though hiring is slowly returning. While claims have slowed, the unemployment rate remained at the historically high level at 13.3%. The calendar also features updates on industrial production and housing starts. Across the pond, the Bank of England is expected to further expand its stimulus program after a report showing that the economy contracted by more than 20% in April. In addition, the European Union will host a fresh round of Brexit talks and a summit to discuss its pandemic recovery fund proposal.

YTD Returns as of EOD Friday 06/12/2020

US Barclays Agg +5.71%, 1.30% yield, -176 bps excess return

US Barclays Corp +3.99%, 2.28% yield, -599 bps excess return

UST 10yr 0.65% yield, -127 bps

S&P 500 3,041, -5.86%

DJIA 25,605, -10.28%

OIL (WTI) $34.47, -47.87%

Gold 1,723, +13.16%

This paper is intended for information and discussion purposes only. The information contained in this publication is derived from data obtained from sources believed by IMTC to be reliable and is given in good faith, but no guarantees are made by IMTC with regard to the accuracy, completeness, or suitability of the information presented. Nothing within this paper should be relied upon as investment advice, and nothing within shall confer rights or remedies upon, you or any of your employees, creditors, holders of securities or other equity holders or any other person. Any opinions expressed reflect the current judgment of the authors of this paper and do not necessarily represent the opinion of IMTC. IMTC expressly disclaims all representations and warranties, express, implied, statutory or otherwise, whatsoever, including, but not limited to: (i) warranties of merchantability, fitness for a particular purpose, suitability, usage, title, or noninfringement; (ii) that the contents of this white paper are free from error; and (iii) that such contents will not infringe third-party rights. The information contained within this paper is the intellectual property of IMTC and any further dissemination of this paper should attribute rights to IMTC and include this disclaimer.